Background

For all the changes in medicine there are some things that seem resolutely stable. Chief among these is the idea that sick people go to doctors’ surgeries or hospitals to be diagnosed and treated. This, the simplest of healthcare tenets, could however begin to be challenged, as one area of imaging begins to be freed.

As identified in Signify Research’s recently published Ultrasound Equipment – World Market Report, the handheld ultrasound market is developing at a rapid pace, but does this growth herald an era of ultrasound at home?

Vendor Impact

- New users driving growth, so vendors can’t depend on existent market share

- To succeed in the handheld ultrasound market, vendors must facilitate inexperienced users

- Vendors must prove continued value post Covid

Market Impact

- Consolidated market in 2019 is ripe for disruption amidst influx of new competitors

- CapEx sales model likely to be challenged in coming years

- Consumerisation could increase the market size manyfold

The Signify View

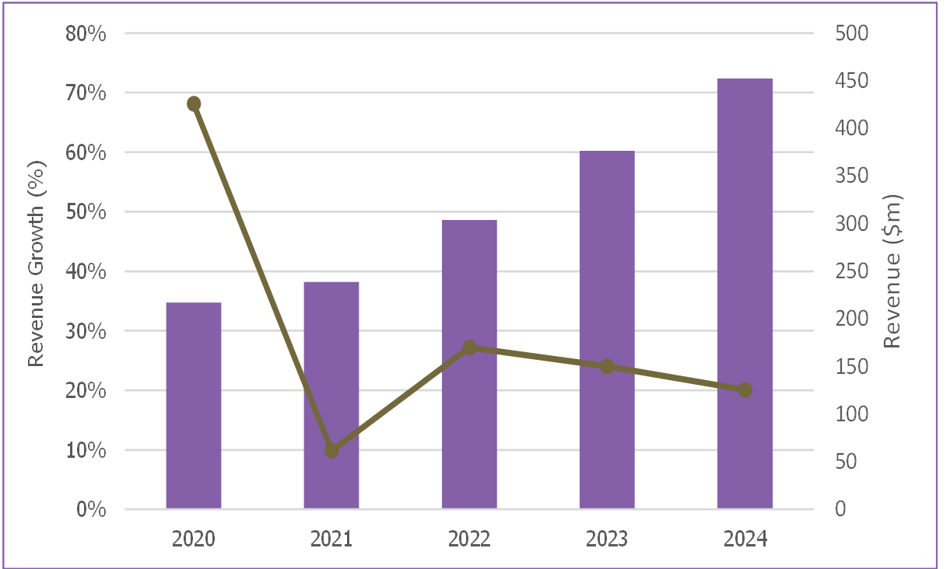

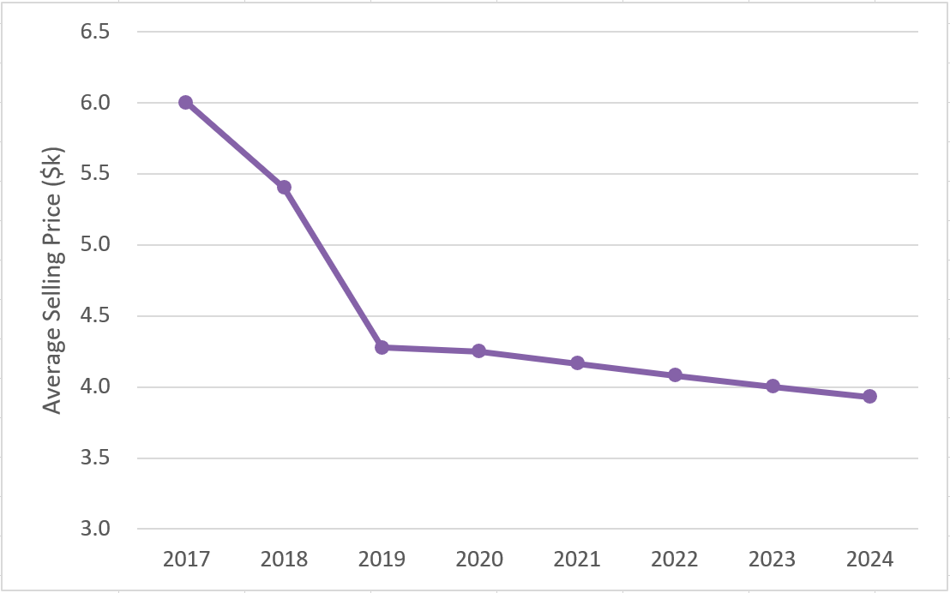

Several things are spurring the growth of the handheld ultrasound market, with one of the most significant being cost. Until recently, a handheld scanner from a trusted vendor was in the region of $5,000 to $10,000. Now, however, largely thanks to the impact of Butterfly Network and its stated aim of democratising medical imaging, scanners can be picked up for as low as $2,000. The combination of improved imaging performance, clinical utility and a lower price has expanded the market opportunity beyond hospital departments to also include office-based clinical specialists. Moving forwards, for a very modest outlay, a primary care physician can equip a surgery with an incredibly useful diagnostic tool. This scenario is predicted to be the biggest mid to long–term growth driver for the product category.

Figure 1: The handheld ultrasound market is set for rapid growth

The Covid pandemic has increased demand for handheld ultrasound massively in 2020, with the technology becoming a frontline diagnostic tool for Covid-19 patients. The availability of affordable and fit-for-purpose handheld scanners has helped hospitals to deal with more patients more quickly – a crucial factor in an exponentially growing pandemic. Handheld scanners, especially wireless versions, are easier to disinfect than traditional cart-based systems and other imaging modalities and infected patients don’t have to move through hospitals to imaging departments, raising the risk of spreading infection. It is forecast, however, that Covid-19 will diminish as a driver of adoption of handheld ultrasound as the worst effects of the pandemic (hopefully) continue to lessen.

But, Covid might also have a longer-term impact on the handheld ultrasound market in other, less direct ways.

Working from home

The Coronavirus pandemic and the subsequent lockdown measures enforced by many of the world’s governments have forced people to do at home what was thought only possible in specifically designed places. Broadcasters appeared suited and booted in front of the filing cabinets in their spare room, tech support calls were interrupted by the barking of wayward dogs as call centre staff worked from their bedrooms. Even politicians weren’t exempt, with parliaments having to pass motions from the safety of members’ living rooms.

In healthcare, in the exceptional circumstances of the worst hit areas of Italy, the home started to become a work environment in other ways, enabled in part by the growing availability of handheld ultrasound systems. In these areas people were being scanned in their homes. Suspected Covid patients no longer had to make difficult journeys to overcrowded emergency departments, where they risked either spreading Covid, or if they weren’t already, becoming infected themselves.

This is just the latest example of a trend which although in its infancy has been steadily gathering pace for several years. Ultrasound is making the jump from a clinical to a domestic setting.

The stage had been set before now, with a number of companies offering the hire of ultrasound machines for the home. Netherlands-based Babywatcher, for example, promises that in conducting a scan, expectant mothers can, “sit back, light the candles and experience the ultimate pregnancy happiness”, with hire of an ultrasound machine being positioned as a perfect pregnancy gift. Baby-Scan meanwhile, suggests pregnant women buy its Baby-Scan Baby-Scanner to “take fun scans at home”. Medical devices are being offered as consumer items. Even the Butterfly IQ, a professional medical device, which warns that it should only be used by qualified practitioners, still features branding and marketing material more reminiscent of a Silicon Valley smartphone than a diagnostic device.

The distinction between serious medical technology and consumer technology was blurred even more this year, when PulseNmore launched in the summer of 2020. The Israeli firm’s device is an ultrasound transducer, which docks with a smartphone, and would look right at home alongside the electric toothbrushes, personal wellness devices and electric shavers that fill people’s bathroom cabinets. What separates the device though, is that as well as “enhancing the pregnancy experience”, Leor Wolff, the Head of Translational Innovation at Clalit Health Services, which is offering the device to its members, claims it will help pregnant women “know about the well-being of their baby”.

Ultrasound has, in just a few years, gone from being a clinical tool to be used in a clinical setting by clinicians, to being a technology that can, in theory at least, be used by anyone, anywhere at any time.

Ultrafreedom

There are several ways in which novice users are being empowered to use a tool that, to this day, many primary care physicians can’t. Firstly, most handled scanners come with built in presets that can be used to quickly garner key measurements. A heart’s auto ejection fraction, or a foetus’s estimated due date for example, can be automatically calculated by the system’s tools.

Another enabler is tele-ultrasound, where live ultrasound images are transmitted through teleconferencing to experts to guide novice users. Interest in tele-ultrasound has been heightened during the Covid pandemic and facilitated by the US FDA’s emergency use authorisation, which has enabled many in the medical field to use ultrasound where they wouldn’t have otherwise. In addition to a typical tele-ultrasound offering, where a trained professional can remotely see the scan and talk a non-trained professional through the process, Butterfly Network have also added an augmented reality tool, which superimposes arrows on a user’s smartphone to visually guide the novice to ensure the scanner itself is positioned correctly.

AI will also play a key part in assisting novices to use ultrasound, both in terms of AI-enabled image capture assistance alongside automated anatomy navigation. Furthermore, AI can also compare the acquired image to standardised criteria, to ensure that it meets clinical standards. The first example of the latter is GE’s Voluson SWIFT which incorporates Intelligent Ultrasound’s ScanNav Assist AI technology. While currently only available on more expensive cart-based systems, it is only a matter of time before this capability cascades down to handhelds.

Finally, in what is perhaps the most consumeresque aid of all, vendors have released simple to understand YouTube tutorials. Novices can follow along, seeing both how to position the IQ scanner, as well as what is displayed on the smartphone screen, which settings to press, and what to look for on the scan itself.

These developments combined with the Coronavirus pandemic and the need to keep people away from hospitals wherever possible means that it is increasingly likely that more ultrasounds are set to be conducted at home. Initially professionals will be responsible, but for people with certain conditions that require regular scans, it might prove safer, more efficient and in the long term cheaper, for people at home to be given a handheld unit, basic training and then left to scan themselves at a given frequency, with the images going directly to a doctor.

Figure 2: Falling prices make handheld scanners more accessible

Further in the future, it is easy to imagine consumers buying scanners themselves, particularly as costs come down and AI-powered instructional software gets better. This is, in fact, where Butterfly’s founder, Jonathan Rothberg would like to see the market head.

“When the first thermometers were made, when the first blood pressure cuffs were made, they were only in hospitals,” he mused when the Butterfly IQ launched.

Hot Topic

A little knowledge, so the saying goes, can be a dangerous thing. This is especially true when that small amount of knowledge is on something as complex as a human body, even applying to the far simpler tools that Rothberg hopes the Butterfly can follow. Take thermometers for example, numerous factors, from genetics to shafts of sunlight and even drafts can undermine the accuracy of a reading.

When being used by non-experts these limitations and inaccuracies can have a huge impact. After all, a medical professional has a wealth of knowledge and experience with which he or she can scrutinise a dubious result, novice users lack this expertise, and are therefore susceptible to drawing incorrect conclusions.

This would no-doubt also be an issue with ultrasound scanners at home. Women could purchase a scanner to see her unborn baby, and lacking any knowledge other than that shared on the scanner’s YouTube channel, could find the heartbeat and assume everything is fine, but miss another indicator of ill health that an expert would pick up. This could be especially prevalent if people depend on the current crop of AI diagnostic tools that are blind to conditions they haven’t been specifically developed to detect.

Conversely, the opposite could also be a problem. Stories of people with indigestion or head colds or whatever spending an hour on the internet and diagnosing themselves with Ebola or dengue fever are now so common as to be a cliché, but imagine the influx of people into emergency rooms if they also had a live image of their heart, lungs or bladder to misread. Imagine the panic and emotional upset of people that think they have found a shadow on the lung of their wives or husbands or struggled to find a baby’s heartbeat.

It seems inevitable that for every legitimate catch, there are going to thousands of misdiagnoses, sending thousands of people to hospitals and clinics each year, and placing even greater demands on the time of already overstretched clinicians.

Homeward Bound

The prevalence of many of these issues will depend on how ultrasound scanners make their way into people’s homes. Afterall, if a scanner is prescribed by a medical specialist who carefully explains the technology and its limitations, it will be thought of very differently than if it is picked up from a supermarket’s health aisle alongside electric toothbrushes and digital scales discounted in the January sales.

Cost will play a big part in deciding which of these paths the technology will take. A price tag of $2,000 might seem cheap to medical professionals used to paying tens of thousands for an ultrasound machine, but to someone at home, that could be more than the cost of their car. As such, the first successful ‘ultrasound at home’ company is likely to be the one that makes it affordable to the mass market. But, the costs of the devices themselves will, at least in the foreseeable future, only be able to fall to a certain price. Regardless of their ubiquity, they will always be precision medical devices with associated costs like calibration and QA which will never be able to be completely nullified, regardless of production efficiencies. So in all likelihood, this means either a subscription model or as part of a broader health service, perhaps from an insurer, rather than an outright purchase, will be what takes the tech mainstream.

This is a good thing. It would bring the cost down to a manageable level for lots of households, getting the devices to people that could benefit from them, but it would also mean that consumers were signing up for a service and not just hardware. It would give them a place to go not only for support during the scan itself, but also with their concerns and their homemade diagnoses. A health plan member could conduct their monthly scan, and, if they saw something unusual, flag it for review (perhaps for a small fee), whereupon it would be assessed by a professional, who could then refer the customer to a supported provider.

From a business side, this would also help the vendors. Instead of growth coming from ever greater volume, at ever lower margins as competition in the market increases, an ultrasound at home subscription service means predictable ongoing revenue, and the ability to scale at a more granular pace. Instead of building a new manufacturing hub based on optimistic sales forecasts, investment could be made with the certainty of sticky and repeatable subscription revenues already in the books.

Another avenue for collecting revenue for handheld vendors is also an app-store option. If a subscription can get the devices in enough hands, it becomes viable for software developers to offer very specific tools. Consumers at home could have a primary reason for having an ultrasound machine, but if they had a sports injury, for example, could well spend a small amount on downloading an AI app to assess it, with the vendor taking a cut.

Sound Outlook

There is still a long way to go before people carrying out their own ultrasound scans at home is as common as them taking their blood pressure or temperature, but the trend is real. Decentralisation is happening, ultrasound has moved from dedicated hospital units, to primary care centres and is making its way to people’s houses via Covid-catalysed health visits.

How this trend develops is reliant on vendors being able to make their products affordable to customers, yet still profitable for themselves. It will also require careful consideration given to the implications and repercussions of allowing a professional tool out in the wild. In the longer term, these considerations, along with the growing adoption of telehealth services (see Signify Research’s Telehealth (Acute, Community and Home) – World 2020 report for more information) will mean a shift toward teleultrasound services, where customers will eventually receive scanners for free as part of a comprehensive ultrasound subscription service, much like today’s smartphone business model, with profits made from tele-ultrasound services and app sales.

Cost is still a barrier to increased adoption, but as that falls, it will just take one vendor, one provider one insurer, just one company with a novel strategy, to strike on the right model, which is both helpful and lucrative, before the floodgates open and ultrasound at home is an everyday occurrence.

Signify Research will be launching a new subscription service “Signify Premium Insights” on 1st November. This insight, and similar future insights, will be behind a paywall from this date and you will have to subscribe to “Signify Premium Insights” to view this content from this time. Please click here for more information on how to subscribe to this service.